Disclaimer:

This website presents the ideas and thoughts of a friend. The information contained within should not be used to make investment decisions. Please contact a licensed certified financial planner before making any financial decisions.

Good Luck, and Good Investing.

Tom from AXA Equitable told me that a 403(b) is an "investment vehicle."

When he said that my next question was "What the heck is an investment vehicle?", but once I understood it, it's actually a really good way to describe what a 403(b) is. Allow me to explain.

An investment vehicle simply means a way to invest money.

For example, if you want to buy a mutual fund, you can go to a financial company and say, "I want to buy 100 shares of mutual fund A", or you can buy the same 100 shares through a 403(b). The 403(b) therefore is the investment vehicle that you are buying your mutual funds through. There are advantages to buying your stocks, or other investments, through a 403(b), and that is what I will try to explain here.

Years ago, the Federal Government came to the realization that they are not going to be able to financially support the retired class forever. Basically, the Fed realized that there was no way that Social Security was going to be able to adequately provide for all people over age 65, especially now that people live longer than ever.

As a result of this realization, the Federal government initiated programs like IRA's, 401(k)'s and 403(b)'s, in order to encourage people to try and fund their own retirement. Many of the people who understand how these plans work have fully funded their own retirement nest egg and to them, social security or a pension is just an extra. That's what I'm trying to do. In order to get people to use IRA's, 401(k)'s and 403(b)'s, the federal government had to come up with some sort of incentive to get people to put money in them.

So what's so special about 403(b)'s? What's the inventive?

There are 2 main incentives, other than saving money, that entice people to put money into a 403(b). They are Tax Deductible Contributions, and Tax Deferred Growth. They are a really big deal by the way and I will try to explain them next.

"Tax deductible contributions" means that when you put money into your 403(b) you get to deduct it from your income taxes. Here's the math.

Example:

Suppose you earn $70,000 per year.

When you approximate your income taxes take 25% of 70,000.

.25*$70,000 = $17,500 in taxes that you will pay this year.

Now suppose you put $10,000 into your 403(b). Your taxable income will be reduced by $10,000.

Now when you approximate your income taxes, you take 25% of 60,000 instead of the $70,000 you actually made.

25*$60,000 = $15,000 in taxes that you will pay this year.

You are now paying $15,000 in taxes this year instead of $17,500. That is an immediate savings of $2,500 that you would have paid to the government but now you don't have to. You get to keep that money for yourself!

The moral to the story: TAX DEFFERED CONTRIBUTIONS ARE GREAT!!!!!! and there aren't many ways to get them. A 403(b) is one way.

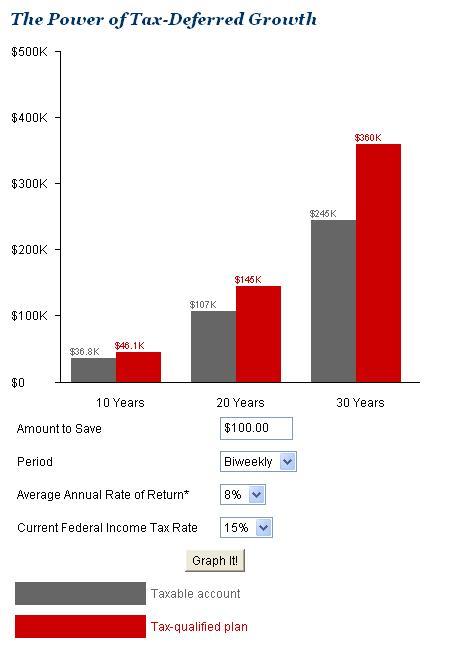

Tax Deferred Growth is a little different and I think a little more complicated. It basically means that you do not need to pay taxes on the growth of your money.

Let's go back to the above example when I said you can just walk into a financial institution and buy 100 shares of a mutual fund A. If during the course of the year, the manager of the mutual fund sells any shares of your mutual fund for more than he paid, he generates what is called capital gains.

Basically whenever a stock is sold for more than it was bought, you earn a profit, that profit is called capital gains. Not surprisingly, when you get capital gains, Uncle Sam wants his piece. At the end of the year when you pay your income taxes, you have to pay tax on your capital gains. Money invested inside a "qualified plan", which is what they call 401(k)'s, IRA's and 403(b)'s, is not subject to capital gains taxes. In other words your investment grows tax deferred. This too is a great thing.

There are some rules associated with 403(b)'s that you need to be familiar with because if you break these rules, the Federal Government gets very upset.

1) You can only contribute to your 403(b) through a payroll deduction.

2) You may only contribute a certain amount to your 403(b) each year. In 2006 you may contribute up to $15,000 unless you are over 50 in which case you can contribute up to $20,000. The rules change every year so get a better source than me for the most up to date contribution information.

3) You may not be able to freely transfer money from one company to another. For example, if you begin your 403(b) with VALIC and you decide to switch to Vanguard, you can not just move your money. You may be eligible to transfer part of your money each year, but if you move the whole thing you will pay a penalty to VALIC. This is just one reason why it is so important to research each company before you decide which one to invest with. For answers to some of your questions about transfers go to the How To Switch page or click here.

4) You can not just go get your 403(b) money whenever you want. A 403(b) is a retirement account and if you take out money too soon you are severely penalized. In most situations, you are allowed to start taking payments from your 403(b) without penalty when you turn 59 1/2, and you must start taking Required Minimum Distributions (RMD's) when you turn 70 1/2. (Let's hope we all make it that far.) There are more rules concerning withdrawls that you should investigate, but these are the basic ones.

5) When you invest money in a 403(b) it can only go into certain types of investments. For example, you may put your money in a mutual fund but it may not be invested in an individual stock. I don't know all the different types of investments it can go in but the two main types are stock funds, also called mutual funds, and bond funds.

Here is where knowledge is power!

There are two types of 403(b)'s.

I REPEAT, THERE ARE 2 TYPES OF 403(b)'s!

(Do you get that this is important.)

The two types of 403(b)'s are the 403(b) Tax Sheltered Annuity (TSA) and the 403(b)(7) Custodial Account. The 403(b)TSA includes a variable annuity and the 403(b)(7) does not include a variable annuity. (Read that again a few times until you understand it. It will be one of the the most important factors you will need to consider when deciding what 403(b) provider to choose. )

A Variable Annuity in a 403(b) is an Insurance Policy. When you sign up for a 403(b) TSA, you are also purchasing an insurance policy. The policy is pretty simple. Basically, the insurance policy guarantees that in the event of your death, your beneficiary will recieve either the total amount of money currently in your account, or, a check for the total amount of money you have invested over time, whichever is greater. Make sense? Maybe not, so let me explain.

Let's assume that for the past 10 years you have been contributing $10,000 each year to your 403(b). (Wouldn't it be nice if we could all do that?) Your principal, the money you have put in, is therefor $100,000. Let's now assume that you die. How much does your beneficiary get?

There are 2 possibilities. One is if your account is currently valued at more than $100,000, and the other is if your account is currently valued at less than $100,000. If you account is currently valued at more than $100,000 your beneficiary gets the whole thing. If your account is currently valued at less than $100,000, your beneficiary will get $100,000. In other words, upon your death, your principal is guaranteed. It sounds like a "can't lose" proposition, but read on.

In a 403(b) TSA, you get this insurance policy, but it's not free. According to the SEC, the average Variable Annuity costs around 1.75% per year, so for your account that has $100,000 you will pay $1750 this year for your life insurance policy. Just for comparison I also have a life insurance policy but it is seperate from my 403(b) and it is called a term life policy. I pay around $715 per year and if I die, my beneficiary receives $2,000,000.

So you understand this better, let's continue with this same example. I don't know how much you know about the stock market, but most people who invest in 403(b)'s invest at least a portion in the stock market. Remember, you have been investing $10,000 for 10 years, do you know what the probability is that your account is worth less than the $100,000 that you put in. Somewhere close to zero! That's not to say the market doesn't go down, it does. And that's not to say that the market doesn't have prolonged periods of decline, it does. But over long periods of time, the market has never gone down. But even so, let's assume the market does terrible over the 10 years you have been investing, what is the worst your account could be? Maybe $70,000 at worst. So let's assume you die after 10 years again, do you remember how much your beneficiary would get? $100,000. But keep in mind, $70,000 of that money is already yours. The insurance company only has to kick in the extra $30,000, so now you are paying around $1000 per year for $30,000 in life insurance. For more information on how Variable Annuities work, I recommend you call your 403(b) TSA rep and review these numbers with him. Be sure to ask him what percent of your 403(b)TSA goes towards the death benefit so you can determine exactly how much your death benefit is costing you this year. That way you will be better able to decide if a Variable Annuity is right for you. While you are on the phone with him, ask him what the principal is on your account and the current balance to find out if you would get any benefit upon your death and one more thing. You may be curious to find out exactly what percent of 403(b) death claims actually pay out more than the principal.

By the way, if you think a 403(b) TSA is right for you, I strongly recommend you buy one.

This is just the beginning of the discussion on what Variable Annuities are. To learn more select the "Variable Annuities" link on the menu to the left.

There is one other thing you get in a TSA that you do not get in a 403(b)(7) and that is a rep who knows and cares about you. I know that sounds like I am trying to poke fun at them but that is only partially true.

The fact of the matter is, your rep really will do things for you that you will have to do for yourself if you get a 403(b)(7). If you sign up for a 403(b)(7) with a company like Vanguard , you will have to pick where your money is invested. In a 403(b) TSA your rep will work with you to make this decision based on your age, risk tolerance etc.

If you invest with a company like Vanguard, you will have to make sure you don't go over the yearly maximum, and you will be responsible for changing your contributions each year. With one of the insurance companies, they will make sure you don't go over the max and they will ask you every year if you want to increase your contributions. This is a legitimate service and is worth something. You need to find out how much you pay for it and decide if it is worth it for you.

You should now have a pretty good idea of what a 403(b) is and you should understand that there are two different types of 403(b), the 403(b)TSA and the 403(b)(7) Custodial Account. If you have decided that you want the Tax Deduction and the Tax Deferred Growth, it is time to learn how to choose which company you want. First take a look at the companies you have available in Wayne, Your Choices in Wayne, and then go to How Do I Pick a Provider.